New media is now old. This year, the internet celebrates its 45th birthday, while online news in the UK has reached adulthood. Any publishing strategy needs to understand that we are now in a ‘three generations in one’ news industry. There are still the legacy products like 'dead tree' newspapers and analogue broadcast but there is also the content re-versioned for online. Then there are the purely 'digital native' enterprises who sprang up fully formed by the internet. One new trend is that those three generations are increasingly combined in interesting ways.

Last year, I wrote in this magazine that newspapers had all accepted the idea of ‘digital first’. This is the idea that even if you make most revenue out of analogue, you must still re-structure your business according to the priorities of digital production and consumption. It is now the time (overdue in fact) to hire developers, publish on demand and design everything for mobile.

The implication of that strategic shift is that content is now King, Queen and Jack of Hearts. In a world where the consumer can easily access what they want directly or through networks, it is the product not the platform that matters if you want to create a sustainable business. The last twelve months have backed that up in spades.

Those who have made the great leap forward might still face the Great Reckoning. If you can’t monetise it, then all the ‘listicles’ and ‘retweets’ in the world won’t pay for your new servers and the re-design let alone the shareholders’ dividend. But while I don’t want to get too cheery, it might be that we are seeing the first rays of a new dawn. After a decade that I have spent following the destruction and re-ordering of journalism, I have never known people to be so (relatively) positive. So what’s going on out there?

A brighter outlook

It is partly about general economic clouds lifting in much of America and Europe. At the same time, media markets are continuing to grow fast in Asia and even in Africa as those regions benefit from improved economies and accelerating internet penetration. So across the world, we can say that we are now past the shock of the new and into the proving phase of the ‘digital native’ generation.

Key to my sense of optimism is that the fresh investment is coming from a variety of sources and is going into many different approaches. We are seeing more new cash but also a commitment to different strategies.

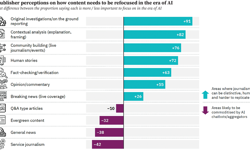

Look at the range of players in the UK alone, from the BBC to BuzzFeed. You can see that there is a lot of poor quality content out there (and much of it on traditional platforms) but I would argue that, overall, the journalism has never been better. Phone-hacking and associated scandals have grabbed the headlines about journalism recently. But go and look at the award-winning investigations of the Guardian, the new Telegraph women’s and football blogs, the Mirror’s new social media streams, the FastFT (and the slow FT), the foreign coverage of the BBC or the much-improved LBC.

But is it sustainable?

New money

One indication is that there is a lot of new money coming into the business in some places. There has been a sudden rush of new owners bringing in new capital in the United States. Pierre Omidyar, the eBay billionaire, is putting aside $250 million to set up First Look Media which promises to combine top individual brands like Glenn Greenwald and Andy Carvin in a network that will deliver – he says – more than the sum of its parts, without getting trapped in the institutional inertia of traditional news media.

It’s not going to be easy for Omidyar to integrate such strongly ‘disruptive’ characters but this is still very much a work in progress. I am told that First Look is currently about internal seminars on structures rather than fine-tuning organisational detail. But in an age where media companies like Google have incredibly low overheads, paradoxically the network advantage for First Look might be NOT to be too managed.

Jeff Bezos first appeared to have invested in the Washington Post as much for cachet as the cash. But already things have cheered up by the banks of the Potomac. It may be that as well as vital funds, he can bring delivery innovation to content in the same way he did for books (and potentially everything else). Key must also be the data that he can combine from Post readers and his global retail network. These days, what you know about your readers might be more valuable than their subscriptions. I am told that Bezos is very much in this for the long haul and sees profit to be made in the rich pickings from the data about readers.

In the UK, the Guardian has also gone for a mixed model. It gets millions from foundations like Gates’ and its Australian office start up was bankrolled by an internet entrepreneur and environmentalist Graeme Wood. Thanks to the well-timed sale of Auto Trader, the Guardian is now a bit like a venerable Oxford college supported by an endowment fund. As it is governed by a trust, this means it still needs to make money to pay the bills but it doesn’t have to make a profit for shareholders. It has had a remarkable impact punching above its weight with a global reach and scale that is the envy of other media organisations. It sells ethics. The kind of political bravery that led to the Snowden publications in the teeth of UK government opposition has placed it as the world’s leading liberal / radical news brand. At the other end of the business model spectrum, The Times claims its tighter paywall model has reached a viable level of subscriptions.

So this is what I mean by ‘three generations in one’. ‘Old’ traditional mainstream media is still there with TV news and dead tree press still the major sources of income. At the same time and in the same organisations, there now is the online content and workflows. But there are also the independent 'digital native' creators.

Thinking like natives

Some publishers have tried to create a digital startup culture within their own walls. European publishing giants Sanoma and Axel Springer have literally invited outsiders in on a competitive basis and picked the best for further investment. Even the dear old BBC has created a News Lab to act as a kind of internal innovation consultancy.

Trinity Mirror has been something of a graveyard for digital innovation in the past. This time, a team of non-Mirror folk were brought in and the early signs are that a variety of initiatives are working. The Telegraph has tried a similar approach with its Babb site for footie fans. The acid test is whether these relatively peripheral exercises can grow scale or act as a model for more widespread implementation. Are they the icing or the cake?

Simultaneously, we are seeing new news ventures such as Nate Silver’s FiveThirtyEight emerge from the mainstream to stand on their own. And then, of course, there are the ‘digital native’ news enterprises that start on their own like BuzzFeed or Vice. Intriguingly as these gain scale they are becoming much more like their more traditional competitors. BuzzFeed has now hired foreign correspondents and produces intelligent, balanced political news as well as the funny quizzes and lists. This move towards the serious might have something to do with research evidence that shows that quality content earns much more advertising revenue per click than traffic bait.

These upstarts are attracting more than just editorial attention from the mainstream. Rupert Murdoch once asked on Twitter, “Who’s heard of Vice Media?” Then a year ago, he bought a $70 million stake.

So the dead tree press may still be sacking staff but it is also hiring new people. Digital revenues don’t match the golden days of the analogue advertising past but they are continuing to rise. The Guardian losses are being slashed, while groups like the Telegraph and Mail report profits. Even parts of the local press are getting their heads back above water. But there are two other massive structural trends that should concern UK papers: the new realities of global competition and the power of the platforms.

The Brits are coming

Global competition is currently going in the UK’s favour as news organisations such as the Guardian and the Mail rush to re-colonise America, Australia and even India. English is still the global language and British journalists have been way ahead of others in occupying that space. However, it’s proving relatively difficult to convert worldwide traffic into revenue. For example, I am told that the Guardian’s antipodean adventure is not likely to make a profit. While its US edition does not yet bring in much either, that is where the money is to be made in the future if the Manchester Guardian can become part of Americans’ reading habits. The key will be turning clicks into real engagement. At some point, too, other global giants such as China are going to start muscling in on these international audiences. And they really do have the funds for a fight.

And the platforms? Well, news organisations used to complain about how the platform giants such as Google and Facebook used their content to attract traffic. They now seem to be more grateful for the attention that the networks can deliver. Search connects content to consumers. Social media integrates material into people’s online lives. They all act as an accelerator to distribution through sharing. These platforms are also incredible tools to create community, to collect content and to foster creativity in the crowd. Any journalist not using something like Tweetdeck, for example, as a basic discovery device shouldn’t be drawing a pay cheque.

But there are now a whole lot more platforms or networks that are emerging and growing rapidly. SnapChat, Instagram and Pinterest have made their way in social media tapping into different consumer groups by generation or gender. They are all now significant players in the news ecology. It all raises the question why legacy media didn’t come up with those models. At the very least, publishers or content creators ought to be thinking about using them and thinking about where that innovation comes from.

Facebook’s $19 billion acquisition of WhatsApp reminds us that digital media has grown up. It is now in that phase where the biggest corporate beasts will snaffle up the tastiest competitors to reinforce their own market dominance. The platforms have much bigger fish to fry. Google is not a search engine anymore. It’s a vast machine for the exploitation of data. Facebook isn’t so much a social network as an online store. The next phase will be all about how the recovering news organisations can fit their content into these new commercial realities.